Think of your homeowners insurance policy as a financial shield, a promise from your insurer to restore your home and your life when the unexpected strikes. For homeowners in Orange County, where your property is one of your most significant investments, this policy is more than just a document—it's the critical defense protecting your home, belongings, and financial future from catastrophe. When a fire, burst pipe, or major storm hits, a well-understood policy is what stands between you and a devastating loss.

Demystifying Your Homeowners Insurance Policy

Let's be honest—insurance policies can be a headache. They're often filled with jargon that feels designed to confuse, not clarify. But you don't need to be an insurance expert to understand what you're paying for. This guide is here to translate that dense policy language into simple, practical knowledge you can use to protect your Southern California home.

As an IICRC Master Certified firm and a licensed general contractor serving Orange County, we've seen firsthand how a solid policy turns chaos into calm. We’ll break down a standard policy, piece by piece, so you know exactly what’s covered. We'll start with the six core parts of a typical HO-3 policy, the most common type for single-family homes, giving you a strong foundation for understanding homeowners insurance coverage.

For broader insights, especially during major life changes, you can also explore these essential insurance tips for a stress-free move.

Your Policy at a Glance

A standard homeowners policy is a package of different coverages bundled together, with each part designed for a specific job. Getting a handle on these pillars is the first step to feeling confident in your protection. Here’s the big picture:

- Property Coverage: This is the heart of your policy. It's designed to pay for repairs to your house and other buildings on your property, and to replace your personal belongings if they're damaged or stolen.

- Liability Coverage: This part protects you financially if someone is injured on your property and you're held responsible, or if you accidentally cause damage to someone else's property.

- Additional Living Expenses: If a covered disaster makes your home unlivable, this coverage helps pay for temporary housing, food, and other costs while your home is being repaired.

For Orange County homeowners, where property values are among the highest in the country, understanding every line of your policy isn't just a good idea—it's a critical strategy for protecting your investment and maintaining your financial stability.

To make this even clearer, the table below breaks down the six core coverages found in most standard HO-3 policies. Think of it as a cheat sheet for your insurance.

Standard Homeowners Insurance Policy at a Glance (HO-3)

| Coverage Type | What It Covers | Common Use Case |

|---|---|---|

| Coverage A: Dwelling | The physical structure of your house and attached structures (like a garage). | Rebuilding your home's walls, roof, and foundation after a fire. |

| Coverage B: Other Structures | Standalone structures on your property, like a shed, fence, or detached garage. | Repairing a fence that was damaged by a fallen tree during a storm. |

| Coverage C: Personal Property | Your belongings, including furniture, electronics, clothing, and other valuables. | Replacing your furniture and electronics after they're destroyed by water damage. |

| Coverage D: Loss of Use | Additional living expenses if your home becomes uninhabitable due to a covered loss. | Paying for a hotel or rental home while your house is being rebuilt after a disaster. |

| Coverage E: Personal Liability | Legal and medical expenses if you are found legally responsible for injuring someone. | Covering medical bills if a visitor slips and falls on your icy driveway. |

| Coverage F: Medical Payments | Medical bills for guests injured on your property, regardless of who is at fault. | Paying for a guest's emergency room visit after they cut their hand in your kitchen. |

Understanding these six components is the key to mastering your homeowners policy and making sure your coverage truly meets your needs.

What to Expect From This Guide

Our goal is simple: to empower you with the confidence to manage your insurance effectively. As an IICRC Master Certified firm and a BBB Torch Award Winner for Ethics, we at Sparkle Restoration have helped countless Orange County families navigate the claims process. We’ve witnessed firsthand how a solid, well-understood insurance policy can bring order and hope to a chaotic situation.

We’ll walk you through everything you need to know, from reading your policy declarations page to filing a claim successfully. This is the foundational knowledge every homeowner needs. If you have immediate questions about insurance and the restoration process, you can find quick answers in our frequently asked questions.

Breaking Down the Core of Your Homeowners Policy

Think of your homeowners insurance policy less like a single document and more like a comprehensive toolkit. Each tool inside is designed to fix a very specific type of problem. For any Orange County homeowner, understanding what each tool does is critical, especially when your property investment is one of the biggest you'll ever make.

Let's unpack these six core coverages one by one, using real-world examples to show how they work together to create a solid financial safety net for you and your family.

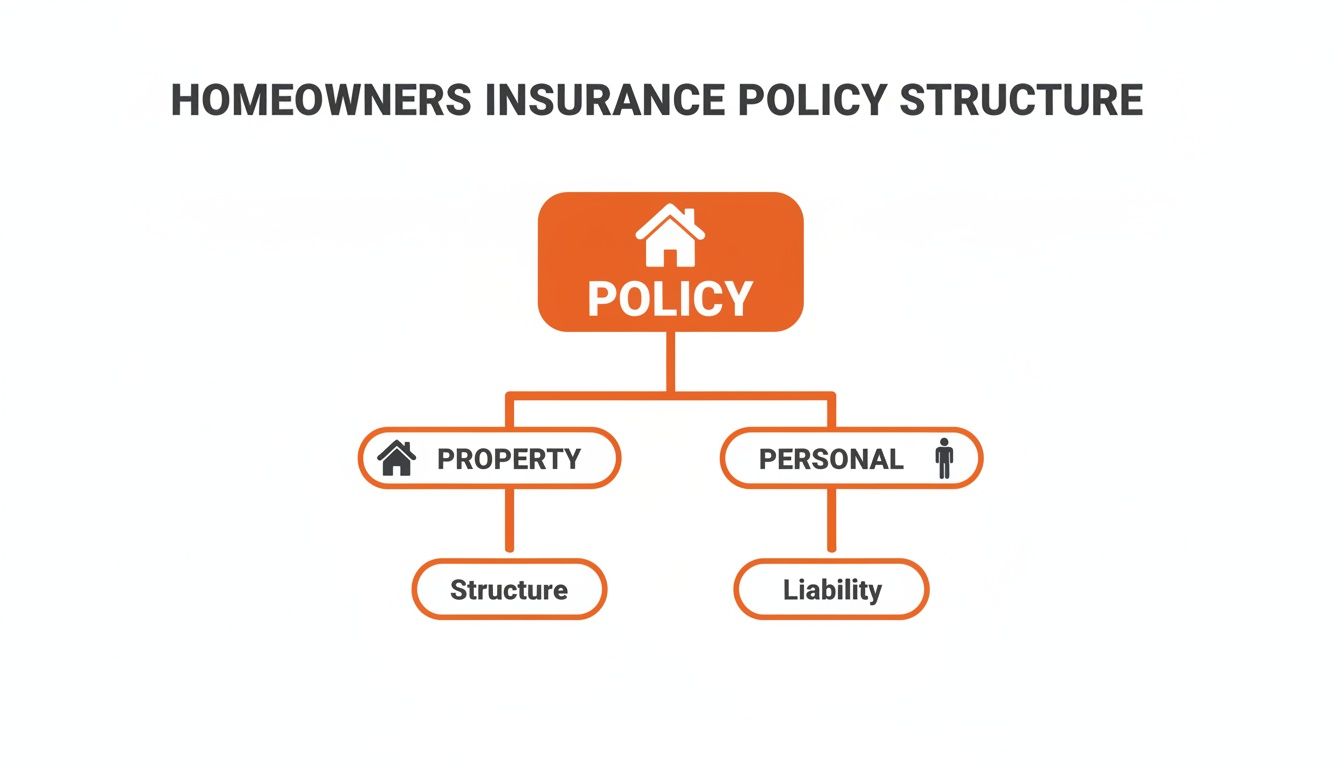

This flowchart gives you a bird's-eye view of how a typical policy is structured, splitting the coverage between protecting your physical property and protecting you personally.

As you can see, the policy branches out to cover everything from the house itself to your personal liability, making sure all your bases are covered.

Coverage for Your Property

The first four parts of your policy are all about protecting the physical things you own—your house and everything in it. They are the foundation of your financial recovery after something goes wrong.

Coverage A Dwelling: This is the big one. It covers the main structure of your house—the walls, roof, foundation, and anything physically attached, like your garage. If a fire sweeps through your Newport Beach home, this is the coverage that pays to rebuild it. The limit isn't based on your home's market value, but on the real-world cost to reconstruct it from the ground up.

Coverage B Other Structures: This part of the policy protects structures on your property that aren't attached to the main house. We're talking about things like a detached guest house, your backyard shed, a fence, or even that custom-built outdoor kitchen you love. Typically, this coverage is automatically set at 10% of your Dwelling (Coverage A) limit.

Coverage C Personal Property: This covers all your belongings inside the house. From your furniture and electronics to your clothes and kitchenware, this is the coverage that helps you replace it all. Imagine a pipe bursts and floods your living room—Coverage C is what you'll use to buy a new couch, TV, and rugs. You can get a better handle on disasters like this by reading our guide on the essentials of water damage restoration.

Coverage D Loss of Use: This coverage is a true lifesaver if a major event, like a fire, forces you out of your home. It's designed to pay for your additional living expenses while your home is being repaired by a team like ours at Sparkle Restoration. Think hotel bills, restaurant meals, and laundry services—the extra costs you incur because you can't live at home.

Replacement Cost vs. Actual Cash Value

A crucial detail hidden in the fine print is how your insurance company values your property when you file a claim. Getting this right can mean the difference between being made whole and coming up financially short.

- Replacement Cost Value (RCV): This is the gold standard. RCV pays to replace your damaged property with a brand-new item of similar kind and quality, with no deduction for age or wear and tear.

- Actual Cash Value (ACV): This option pays you what your damaged item was worth the moment before it was destroyed. It's the replacement cost minus depreciation. So, if your five-year-old laptop gets fried, ACV pays you what a five-year-old laptop is worth today, not the cost of a new one.

Key Takeaway: Always advocate for Replacement Cost coverage for both your dwelling and your personal property. It’s the only way to ensure you can fully rebuild and replace your belongings without dipping into your own savings.

Coverage for Your Personal Liability

The last two parts of your policy pivot from protecting your property to protecting you from lawsuits. In our litigious society, this coverage is absolutely essential.

Coverage E Personal Liability: This is your financial defense if someone gets hurt on your property and decides to sue you. It covers your legal fees and any damages a court might award, up to your policy limit. If a guest slips on a wet tile in your Irvine home and files a lawsuit, this coverage kicks in to handle the legal fallout.

Coverage F Medical Payments to Others: Think of this as "goodwill" coverage. It pays for smaller, no-fault medical bills if a guest is injured on your property. It’s designed to handle minor incidents quickly—like a friend cutting their hand in your kitchen—to hopefully prevent them from escalating into a large liability claim. It pays for their trip to urgent care, regardless of who was at fault.

The need for this kind of protection is clear when you look at the numbers. The global home insurance market hit USD 234.6 billion in 2024, pushed by soaring property values. Here in the U.S., which accounts for about USD 73 billion of that, homeowners in high-value areas like Orange County face unique risks. For a luxury home in Newport Beach, every $100,000 increase in dwelling coverage can bump up premiums by $400-$500 a year, making it vital to know exactly what you're paying for.

What Your Standard Policy Does Not Cover

A standard homeowners policy provides a robust shield against many common disasters, but it is not an impenetrable fortress. One of the most critical parts of understanding homeowners insurance coverage is knowing its limits. Many homeowners mistakenly assume their policy is a catch-all, only to discover dangerous gaps when a specific type of disaster strikes.

For owners of high-value homes in Orange County, these gaps can be particularly costly. Certain perils, especially those common to Southern California, are almost always left out of a standard HO-3 policy. Recognizing these exclusions is the first step toward building a truly secure financial safety net for your property.

Common Perils Excluded from Standard Policies

While your policy covers events like fire and theft, it draws a hard line at others. Think of these exclusions as specific events your insurer has decided are too widespread, too predictable, or simply too expensive to bundle into a standard package.

Here are the major exclusions every California homeowner should be aware of:

- Earthquakes: Damage from any kind of earth movement—including tremors, quakes, and landslides—is a universal exclusion in standard homeowners policies. Given California's seismic activity, this is a massive gap that requires a separate, dedicated earthquake insurance policy.

- Floods: No standard policy will cover damage from flooding caused by rising bodies of water. This means overflowing rivers, storm surges, or even heavy, prolonged rain that saturates the ground won't be covered. You need a separate policy, usually from the National Flood Insurance Program (NFIP) or a private insurer.

- Sewer & Drain Backup: This is a common and unpleasant surprise. If a municipal sewer line backs up into your home or your sump pump fails, the resulting water damage is not covered by a standard policy.

- Neglect or Lack of Maintenance: Insurers expect you to keep your property in good shape. Gradual damage, like mold from a slow, unrepaired leak or a roof that fails due to old age, will almost always be denied. Proactive maintenance is key, and our guide on how to leak-proof your home offers valuable prevention tips.

Closing Coverage Gaps with Endorsements

Fortunately, you are not powerless against these gaps. You can customize your policy using an endorsement, also known as a rider. It's essentially an add-on to your existing policy that provides coverage for risks not included in the base plan. Think of them as precision tools for tailoring your insurance to your specific needs.

For owners of high-value homes in communities like Irvine and Newport Beach, endorsements are not just optional extras—they are essential components of a responsible risk management strategy, protecting unique assets and lifestyle.

Let's explore a few of the most valuable endorsements that can make a world of difference.

Essential Add-Ons for Orange County Homeowners

Think of these endorsements as plugging the most common—and most expensive—holes in your insurance armor. Each one addresses a specific vulnerability that could otherwise lead to tens of thousands of dollars in out-of-pocket costs.

Water Backup and Sump Pump Overflow: This is one of the most important endorsements you can buy. It specifically covers damage caused by water backing up through sewers or drains or from a failed sump pump. Given the aging infrastructure in many areas, this coverage is a must-have.

Scheduled Personal Property: Your standard policy limits coverage for high-value items like jewelry, fine art, and collectibles to a surprisingly low amount, often just $1,500. A scheduled property endorsement insures these items for their full appraised value, offering much broader protection against theft or damage.

Ordinance or Law Coverage: If your home is significantly damaged, you'll likely be required to rebuild it to current, stricter building codes. A standard policy only pays to restore your home to its previous condition. This endorsement pays the extra cost—which can be substantial—to bring your home up to modern code during reconstruction.

By strategically adding these endorsements, you can transform a standard policy into a customized plan that reflects the true value of your home and possessions, ensuring you’re truly prepared for the unexpected.

The Financial Realities of Premiums and Claims

Let's talk about the money side of homeowners insurance. It can often feel like you're trying to hit a moving target. Premiums seem to creep up every year, and figuring out why is a huge part of understanding homeowners insurance coverage. This isn't just your insurer randomly hiking prices; it’s a direct response to some major economic and environmental shifts that affect the entire industry—and ultimately, your wallet.

For those of us with high-value homes, especially in places like Orange County, these changes hit even harder. The cost to rebuild a house today is worlds away from what it was just a few years back, thanks to skyrocketing material prices and ongoing labor shortages. At the same time, we're seeing more severe weather, from wildfires to intense storms, which means insurance companies are paying out more claims, more often.

Why Your Premiums Are on the Rise

At its core, insurance is all about shared risk. When the risk for the entire group goes up, the cost for everyone in that group must follow. Insurers are having to completely rethink their pricing to deal with a new reality where disasters are more frequent and rebuilding costs are through the roof.

The numbers don't lie. Homeowners insurance premiums across the U.S. have shot up, with new policies in 2025 averaging $1,966. That's a 9.3% jump from 2024, which came right after a massive 18.8% surge the year before. This isn't just inflation; it's a cumulative 40.4% increase over six years, and high-risk states like California are feeling the brunt of it. On top of that, deductibles have gotten much bigger, placing more of the immediate financial weight on you after a disaster. For a deeper dive, you can check out the full report on 2025 home insurance trends on matic.com.

Actionable Strategies to Manage Rising Costs

While you can't stop inflation or change the weather, you're not powerless. You can take smart, proactive steps to get a handle on your insurance costs without gutting your protection. It’s all about making strategic choices that fit your budget and comfort level with risk.

Here are a few moves that actually work:

Optimize Your Deductible: This is a classic for a reason. A higher deductible usually means a lower premium. Bumping your deductible from $1,000 to $2,500, for example, can lead to real savings. The trick is to pick a number you could comfortably write a check for if you needed to file a claim tomorrow.

Install Protective Devices: Insurance companies love to see homeowners taking preventative measures. Installing things like monitored security systems, smoke detectors, and automatic water shut-off devices can often earn you some nice discounts on your premium.

Bundle Your Policies: This is one of the easiest wins. Most insurers will give you a multi-policy discount if you bundle your home and auto insurance together. It’s a simple way to lower your total insurance bill.

Crucial Insight: Your Dwelling Coverage (Coverage A) must reflect today's rebuilding costs, not your home's market value. Underinsuring your home to save on premiums is a dangerous gamble that can leave you financially exposed after a total loss.

Getting a handle on these costs isn't just about saving money today; it's a vital part of a larger financial plan focused on reducing financial uncertainty. It puts you in the driver's seat, allowing you to make informed decisions that protect your biggest asset for the long haul. And if you do find yourself needing to file a claim, being prepared is half the battle; get a head start by learning about your rights during an insurance claim on our blog.

How to Navigate the Property Damage Claims Process

When your home is hit by a fire, flood, or major storm, the moments afterward can feel like a total whirlwind. It’s disorienting and incredibly stressful. But knowing the right steps can turn that chaos into a structured, manageable recovery process. Successfully navigating a property damage claim really boils down to three things: acting fast, documenting everything, and communicating clearly with your insurer and your restoration team.

This is where your path to getting back to normal begins. By following a clear roadmap, you can protect your property from further harm, advocate for your rights as a policyholder, and ensure you receive the full and fair settlement you deserve. The goal is to move from damage control to complete restoration with confidence.

Immediate Steps After a Property Damage Incident

Before you even think about insurance paperwork, your number one priority is safety. Make sure everyone is out of harm's way and call emergency services if needed. Once the immediate danger has passed, your focus should shift to two things: preventing more damage and documenting the scene.

These first few actions are absolutely critical. They lay the groundwork for a smooth and successful insurance claim down the road.

Prioritize Safety and Mitigate Further Loss: First, make sure the property is safe to enter. Then, take whatever reasonable steps you can to stop the damage from getting worse. This might mean throwing a tarp over a hole in the roof or shutting off the main water valve after a pipe bursts. Insurers expect you to act responsibly to protect your property from additional loss.

Document Everything Meticulously: This is arguably the most important step you can take. Grab your smartphone and take extensive photos and videos of all damaged areas and affected belongings. Get wide shots to show the overall scope of the damage, then get close-ups of specific items. This visual evidence is invaluable when it's time to file your claim.

Contact Your Insurance Agent Promptly: Notify your insurance company or agent about what happened as soon as you can. They’ll give you a claim number and assign an adjuster, who will be your main point of contact. Be ready to give them a clear description of what happened.

Working with Your Insurance Adjuster

The insurance adjuster is a key figure in this whole process. Their job is to investigate the loss, assess the extent of the damage, and determine how much the insurance company will pay out. It's essential to be prepared for their visit and understand their role.

The adjuster will schedule a time to come inspect your property, look over your documentation, and talk to you about the incident. Your detailed photos and videos will be crucial here, especially if some damage gets cleaned up before they arrive. Be honest and thorough, but always remember: the adjuster works for the insurance company, not for you.

A trusted, IICRC-certified restoration contractor like Sparkle Restoration Services can be your greatest advocate. We work directly with your insurance company, using industry-standard pricing and detailed documentation to ensure your claim is fair, accurate, and comprehensive, bridging the gap between you and the insurer.

Partnering with a Professional Restoration Contractor

Once your claim is filed, the next move is to bring in a professional to handle the cleanup and repairs. This is not the time for a DIY project. An experienced restoration company does a lot more than just fix the physical damage; they manage the entire project, from the initial assessment all the way through to final reconstruction.

As a licensed general contractor and restoration expert, Sparkle coordinates every single aspect of your recovery. We provide your adjuster with a detailed scope of work, a precise estimate, and ongoing progress reports. This professional partnership streamlines everything, prevents delays, and ensures all repairs meet the highest quality and safety standards. We handle the complexities so you can focus on getting your life back.

It's also important to recognize that the claims environment is changing. Climate change is dramatically reshaping the insurance landscape. U.S. natural disaster losses have soared from $30.8 billion in 2013 to $79.6 billion in 2023. This has led to premium hikes and even caused some insurers to pull out of high-risk markets, like the wildfire-prone areas of California. For Orange County homeowners, this makes a well-managed claim more critical than ever. You can discover more insights about how insurers are adapting to new climate risks on deloitte.com.

Your Partner in Protection and Restoration

True protection for your home starts with knowing what you're up against and ends with having a trusted partner in your corner. We hope this guide has given you a much clearer picture of your homeowners insurance coverage, from the nuts and bolts of your policy to the often-stressful claims process. Being proactive is always your best, and first, line of defense.

But when disaster does strike, that’s when having an expert on your side really counts.

At Sparkle Restoration Services, we’re more than just a contractor; we're your advocate when you need one most. We bring IICRC Master Certified expertise and an award-winning commitment to ethics to every job in Orange County. Our team knows how to work directly with insurance companies, making sure the entire restoration process is handled with the precision and integrity it deserves.

As a BBB Torch Award Winner for Ethics, we’re built on a foundation of transparent communication and superior work. Our job is to turn chaos into calm when you’re facing the unexpected.

For 24/7 emergency response or to simply get advice on protecting your home, trust the team dedicated to restoring your peace of mind. Learn more about our complete restoration and remodeling services and see how we can help.

Frequently Asked Questions About Homeowners Insurance

Going through the fine print of a homeowners policy can feel like learning a new language. To help connect the dots, we've put together some plain-English answers to the questions we hear most often from homeowners right here in Orange County. Think of this as a practical cheat sheet for real-world situations.

How Often Should I Review My Homeowners Insurance Policy?

We recommend a full policy review with your agent at least once a year. Life moves fast, and your insurance coverage needs to keep pace.

More importantly, certain life events should trigger an immediate call to your agent. Did you just finish a major home renovation? Buy a valuable piece of art or jewelry? These are the moments when your old coverage might not be enough. An annual check-in ensures your dwelling and personal property limits are high enough to fully protect what you own today.

Will Remodeling My Kitchen or Bathroom Affect My Insurance Coverage?

Yes, absolutely. A high-end kitchen or bathroom remodel isn't just an aesthetic upgrade—it significantly boosts your home's value and, with it, the cost to rebuild. The Dwelling Coverage (Coverage A) on your current policy is based on your home's value before the project, which means it will likely fall short afterward.

It's critical to let your insurance agent know before the first hammer swings. They can adjust your coverage limits to make sure your beautiful new investment is fully protected from day one. If you wait, you could find yourself dangerously underinsured.

Does My Homeowners Policy Cover Mold Damage?

This is a tricky one, and the answer is almost always, "it depends." Most standard policies will only cover mold damage if it’s the direct result of a sudden, accidental event that’s already covered—like a burst pipe that you address right away.

However, coverage is almost always excluded if the mold grew because of a gradual problem like a slow leak, poor maintenance, or high humidity. Because this exclusion is so common, many insurers offer a special add-on, called a mold remediation endorsement, which buys back a limited amount of coverage. Given how costly mold removal can be, this is an essential conversation to have with your agent.

At Sparkle Restoration Services, we believe that an informed homeowner is an empowered one. If you’ve suffered property damage and need an expert to help you navigate the entire restoration and insurance claims maze, our IICRC-certified team is here to help 24/7.

Contact us today for a consultation and get the peace of mind that comes from having a true professional on your side.

Ready to create a space that’s as beautiful as it is functional? Schedule your complimentary design consultation today by visiting Ready to Work with Sparkle?